Our 31 page EngineerOnomics industry report contains the latest extensive competitive intelligence analysis and 2018-2025 Outlook of the Turkey Residential Construction Industry. It features an in-depth coverage of the competitive power of different actor segments through our Five Forces Assessment. Key players are suppliers, buyers, competitors, new entrants, and substitute product players. We quantify the power of the most relevant underlying sources of each of these five forces such as switching costs, storage costs, barriers to entry etc, and present the scores of these multivariate drivers through a radar chart. Additionally, our report contains an overview of economic data showing the industry market performance over the last 5-6 years, a statistical forecast for the coming 5 years, a qualitative outlook for the year 2025, key annual financial ratios, key HR data as well as an overview of adopted business strategies of the main companies within the Turkey Residential Construction Industry, including a brief geo-political analysis. The report ends with a general outline of relevant macro-economic indicators and an overview of the main trade

Keywords: Construction, Residential, Real Estate, Machinery, Raw materials, cement, beton, Turkey, Turkish, competitive intelligence, market intelligen ce, industry insights,

industry profitability, 5 forces analysis, five forces, buyer power,

supplier power, barriers to entry, competitive rivalry, emerging

markets, batteries, Covid-19, strategic planning, market volume, market

sizing, market assessment, forecasting, foresight, predictive analytics,

competitive landscape, competitive environment, threats of substitutes,

business strategy, competitive strength, competitive advantage,

competitive intensity, threats and opportunities, strengths &

weaknesses, SWOT, macroeconomics, political economy, statistics, data

analytics, market entry, finance, competition, market opportunities,

strategic positioning, developments, performance, business development,

strategic alliances, strategic negotiations, bargaining power, sales,

research quantitative research, qualitative research, interviewing,

surveying, benchmarking, product development, research &

development, mergers & acquisitions, pricing, data analytics, data

science, segmentation, supply-demand, product development, innovation

management, risk

Our 30 page EngineerOnomics industry report contains the latest extensive competitive intelligence analysis and 2018-2025 Outlook of the Turkey GAS Utility Industry. It features an in-depth coverage of the competitive power of different actor segments through our Five Forces Assessment. Key players are suppliers, buyers, competitors, new entrants, and substitute product players. We quantify the power of the most relevant underlying sources of each of these five forces such as switching costs, storage costs, barriers to entry etc, and present the scores of these multivariate drivers through a radar chart. Additionally, our report contains an overview of economic data showing the industry market performance over the last 5-6 years, a statistical forecast for the coming 5 years, a qualitative outlook for the year 2025, key annual financial ratios, key HR data as well as an overview of adopted business strategies of the main companies within the Turkey GAS Utility Industry, including a brief geo-political analysis. The report ends with a general outline of relevant macro-economic indicators and an overview of the main trade

Keywords: GAS, Utility, Energy, Power, Heating, Turkey,

competitive intelligence, market intelligen ce, industry insights,

industry profitability, 5 forces analysis, five forces, buyer power,

supplier power, barriers to entry, competitive rivalry, emerging

markets, batteries, Covid-19, strategic planning, market volume, market

sizing, market assessment, forecasting, foresight, predictive analytics,

competitive landscape, competitive environment, threats of substitutes,

business strategy, competitive strength, competitive advantage,

competitive intensity, threats and opportunities, strengths &

weaknesses, SWOT, macroeconomics, political economy, statistics, data

analytics, market entry, finance, competition, market opportunities,

strategic positioning, developments, performance, business development,

strategic alliances, strategic negotiations, bargaining power, sales,

research quantitative research, qualitative research, interviewing,

surveying, benchmarking, product development, research &

development, mergers & acquisitions, pricing, data analytics, data

science, segmentation, supply-demand, product development, innovation

management, risk

Keywords: Renewables, Energy, Power, Sustainability, CleanTech, GreenTech, Wind Energy, Wind Turbines, Solar Energy, PV, Hydroelectrics, Hydrogen, Graphene, Microgrids, Selfgeneration, Electric Vehicles, Turkey, Turkish, Marmara region, competitive intelligence, market intelligen ce, industry insights, industry profitability, 5 forces analysis, five forces, buyer power, supplier power, barriers to entry, competitive rivalry, emerging markets, batteries, Covid-19, strategic planning, market volume, market sizing, market assessment, forecasting, foresight, predictive analytics, competitive landscape, competitive environment, threats of substitutes, business strategy, competitive strength, competitive advantage, competitive intensity, threats and opportunities, strengths & weaknesses, SWOT, macroeconomics, political economy, statistics, data analytics, market entry, finance, competition, market opportunities, strategic positioning, developments, performance, business development, strategic alliances, strategic negotiations, bargaining power, sales, research quantitative research, qualitative research, interviewing, surveying, benchmarking, product development, research & development, mergers & acquisitions, pricing, data analytics, data science, segmentation, supply-demand, product development, innovation management, risk

Keywords: Renewables, Energy, Power,

Sustainability, CleanTech, GreenTech, Wind Energy, Wind Turbines, Solar

Energy, PV, Hydroelectrics, Hydrogen, Graphene, Microgrids,

Selfgeneration, Electric Vehicles, China, Chinese, Marmara region,

competitive intelligence, market intelligen ce, industry insights,

industry profitability, 5 forces analysis, five forces, buyer power,

supplier power, barriers to entry, competitive rivalry, emerging

markets, batteries, Covid-19, strategic planning, market volume, market

sizing, market assessment, forecasting, foresight, predictive analytics,

competitive landscape, competitive environment, threats of substitutes,

business strategy, competitive strength, competitive advantage,

competitive intensity, threats and opportunities, strengths &

weaknesses, SWOT, macroeconomics, political economy, statistics, data

analytics, market entry, finance, competition, market opportunities,

strategic positioning, developments, performance, business development,

strategic alliances, strategic negotiations, bargaining power, sales,

research quantitative research, qualitative research, interviewing,

surveying, benchmarking, product development, research &

development, mergers & acquisitions, pricing, data analytics, data

science, segmentation, supply-demand, product development, innovation

management, risk

Our 57 page EngineerOnomics industry report contains the latest extensive competitive intelligence analysis and 2019-2025 Outlook of the China Car Manufacturing Industry. It features an in-depth coverage of the competitive power of different actor segments through our Five Forces Assessment. Key players are suppliers, buyers, competitors, new entrants, and substitute product players. We quantify the power of the most relevant underlying sources of each of these five forces such as switching costs, storage costs, barriers to entry etc, and present the scores of these multivariate drivers through a radar chart. Additionally, our report contains an overview of economic data showing the industry market performance over the last 5-6 years, a statistical forecast for the coming 5 years, a qualitative outlook for the year 2025, key annual financial ratios, key HR data as well as an overview of adopted business strategies of the main companies within the China Car Manufacturing Industry, including a brief geo-political analysis. The report ends with a general outline of relevant macro-economic indicators and an overview of the main trade associations of the Germany Car Manufacturing Industry.

Keywords: Car, Manufacturing, Passenger Vehicles, Automotive, Hybrid, Electric Vehicles, Gasoline, China, Chinese, Geely, competitive intelligence, market intelligence, industry insights, industry profitability, 5 forces analysis, buyer power, supplier power, barriers to entry, competitive rivalry, emerging markets, power drive, drivetrain, hydrogen, batteries, gas, autonomous vehicles, autonomous driving, ADAS, automization, robotization, distribution & transportation, commodities, environmental regulation, Covid-19, strategic planning, market volume, market sizing, market assessment, forecasting, foresight, predictive analytics, competitive landscape, competitive environment, threats of substitutes, business strategy, competitive strength, competitive advantage, competitive intensity, threats and opportunities, strengths & weaknesses, SWOT, macroeconomics, political economy, statistics, data analytics, market entry, finance, competition, market opportunities, strategic positioning, developments, performance, business development, strategic alliances, strategic negotiations, bargaining power, sales, research quantitative research, qualitative research, interviewing, surveying, benchmarking, product development, research & development, mergers & acquisitions, pricing, data analytics, data science, segmentation, supply-demand, product development, innovation management, risk

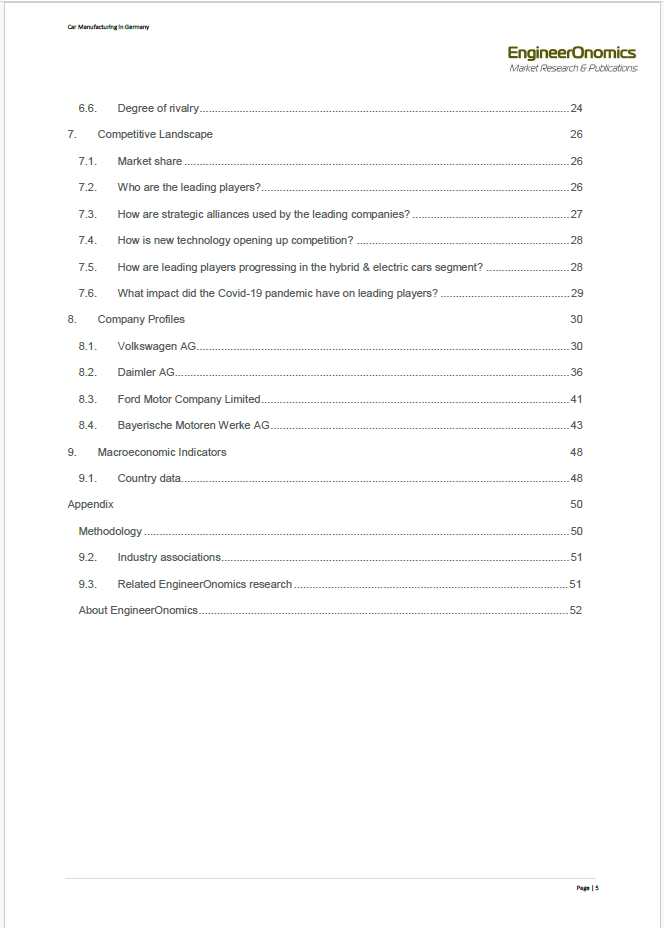

Our 52 page EngineerOnomics industry report contains the latest extensive competitive intelligence analysis and 2021-2025 Outlook of the Germany Car Manufacturing Industry. It features an in-depth coverage of the competitive power of different actor segments through our Five Forces Assessment. Key players are suppliers, buyers, competitors, new entrants, and substitute product players. We quantify the power of the most relevant underlying sources of each of these five forces such as switching costs, storage costs, barriers to entry etc, and present the scores of these multivariate drivers through a radar chart. Additionally, our report contains an overview of economic data showing the industry market performance over the last 5 years, a statistical forecast for the coming 5 years, a qualitative outlook for the year 2025, key annual financial ratios, key HR data as well as an overview of adopted business strategies of the main companies within the Germany Car Manufacturing Industry, including a brief geo-political analysis. The report ends with a general outline of relevant macro-economic indicators and an overview of the main trade associations of the Germany Car Manufacturing Industry.

Keywords: Car, Manufacturing, Passenger Vehicles, Automotive, Hybrid, Electric Vehicles, Gasoline, Germany, German, competitive intelligence, market intelligence, industry insights, industry profitability, 5 forces analysis, buyer power, supplier power, barriers to entry, competitive rivalry, emerging markets, power drive, drivetrain, hydrogen, batteries, gas, autonomous vehicles, autonomous driving, ADAS, automization, robotization, distribution & transportation, commodities, environmental regulation, Covid-19, strategic planning, market volume, market sizing, market assessment, forecasting, foresight, predictive analytics, competitive landscape, competitive environment, threats of substitutes, business strategy, competitive strength, competitive advantage, competitive intensity, threats and opportunities, strengths & weaknesses, SWOT, macroeconomics, political economy, statistics, data analytics, market entry, finance, competition, market opportunities, strategic positioning, developments, performance, business development, strategic alliances, strategic negotiations, bargaining power, sales, research quantitative research, qualitative research, interviewing, surveying, benchmarking, product development, research & development, mergers & acquisitions, pricing, data analytics, data science, segmentation, supply-demand, product development, innovation management, risk

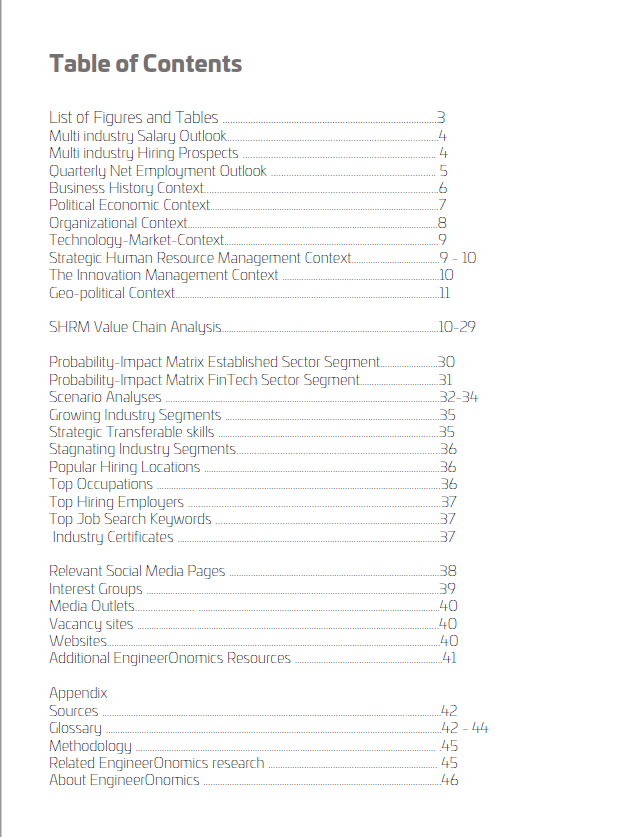

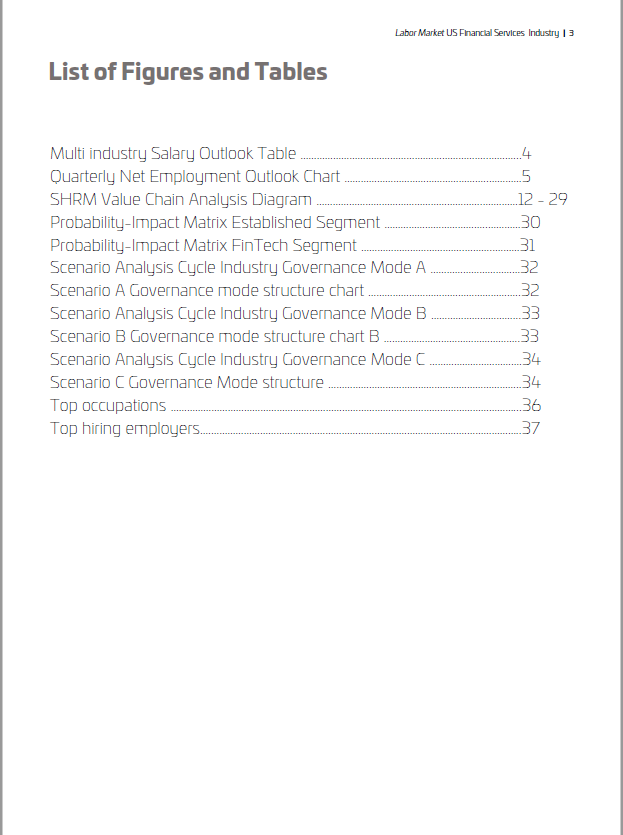

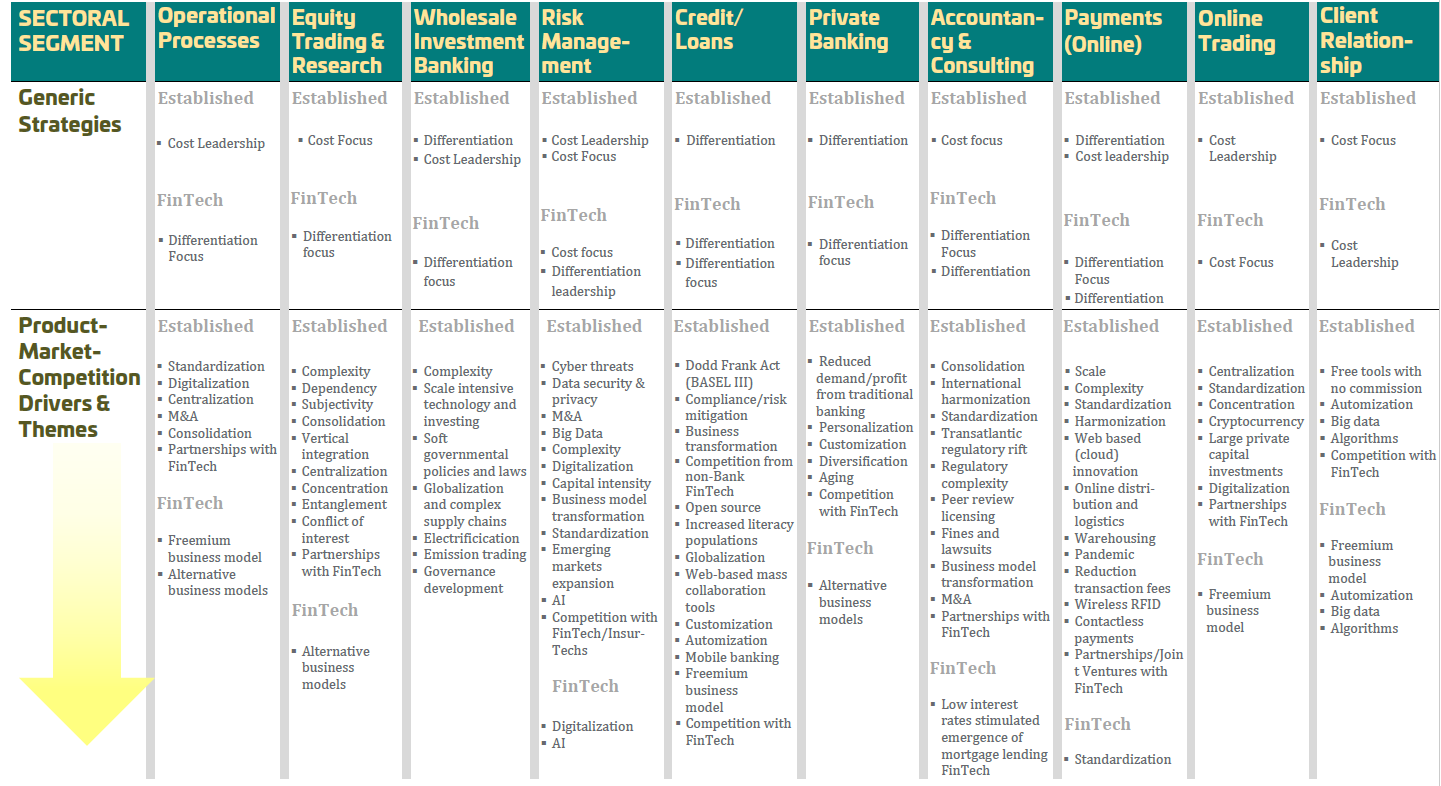

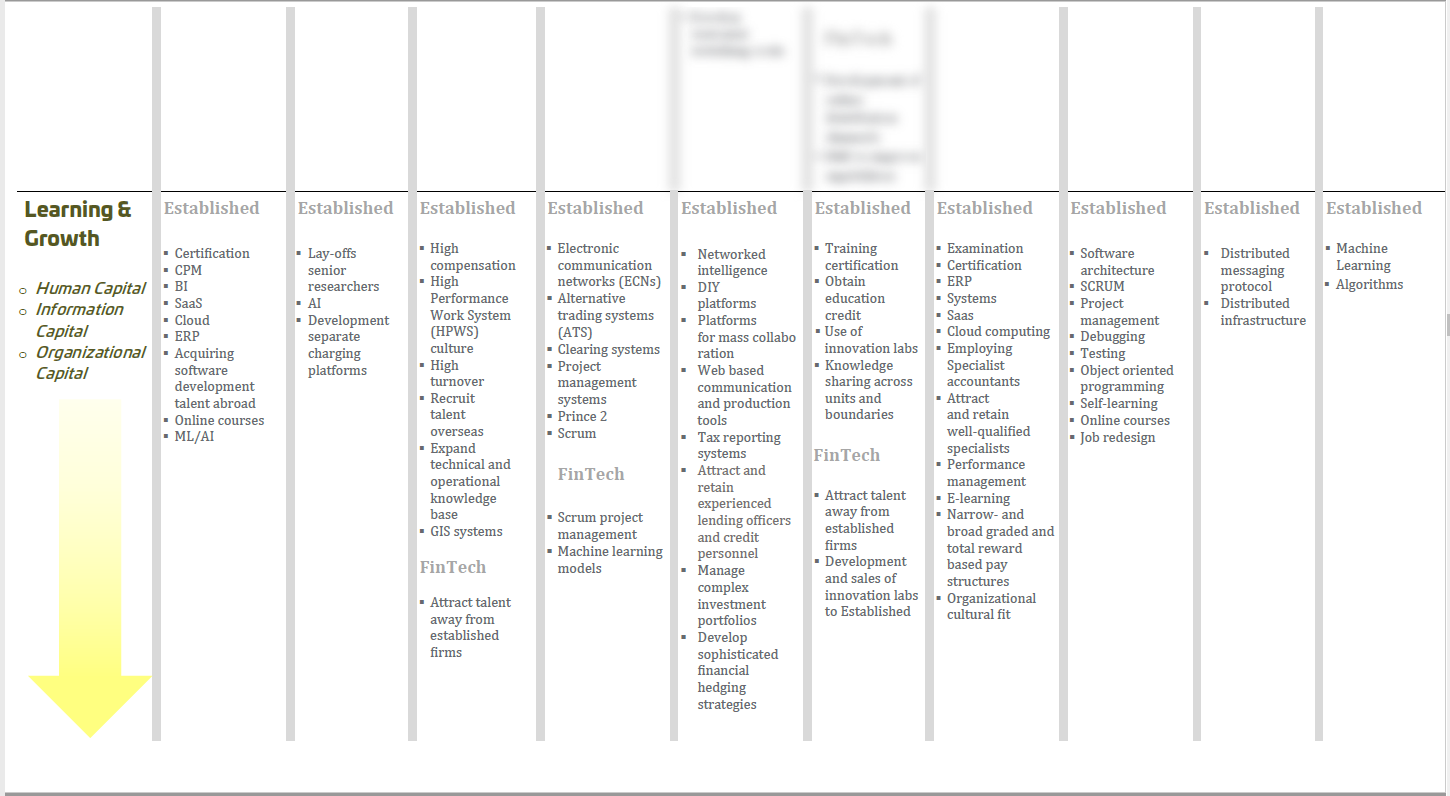

This 46 page report contains the coverage of our strategic forecast survey and assessment of the United States Financial Services labor market 2022 - 2027. It features our quantitative survey results in terms of key US financial services employment market metrics as well as advanced in-depth qualitative analysis. Our qualitative analysis includes an extensive and detailed Strategic Human Resource Management (SHRM) value chain analysis, Probability-Impact Matrix (PIM), Scenario Analysis, a multi-dimensional examination of the external business environment etc. Our quantitative assessment includes the current state of affairs as well as outlook projection in terms of salary growth expectations, top hiring industry segments, strategic transferrable competencies etc. This research and publication is produced for HRM practitioners, management consultants, investment strategists, L&D professionals, and last but not least career professionals. Our intelligence can be applied for purposes of strategic human resource planning, workforce planning, competency management, organizational design, career management, career planning etc.

The United States Financial Services Labor Market Strategic Forecast Survey 2022 is part of a series of research surveys that EngineerOnomics has conducted across various US industry employment markets in association with our TechRuiting© HRM consulting and recruitment practice.

Keywords: Labor Market, Industry Survey, Strategic Research, Employment Services, Human Resources, Career Management, Career Planning, Human Resources, Financial Services, United States, quantitative research, qualitative research, interviewing, FinTech, start-up, Investment Banking, private equity, venture capital, digital assets, investment research, stock trading, institutional investing, asset management, buy-side, sell-side, Forecast, Outlook, Strategic Management, Innovation Management, Competency Management, Job Design, Strategic Mapping, Business Strategy, Value Chain, PESTEL, market analysis, industry assessment, competitive intelligence, market intelligence, industry insights, strategic planning, HR analytics, scenario planning, scenario analysis probability-impact, statistics, industry profiling, SWOT, macroeconomics, political economy, statistics, data analytics, market opportunities, strategic positioning, human capital, intangible assets, HR performance, benchmarking, best practices, continuous improvement, data science, segmentation, risk management, geopolitics, political economy, business history, organizational design, employee skills, employers, salaries, salary, emerging markets, SMBs, performance management, value proposition, differentiation, learning & development, supply chain, value chain, strategy map, HR systems, HR planning, people analytics, HRTech, HR Intelligence, job applications, personal development, digital platforms, e-ecommerce, socio-economics, insitutional economics, competitiveness, profitability, execution, implementation, stategy implementation, data democrotization, entrepreneurship

This 50 page industry report contains the latest extensive competitive intelligence analysis of the Russian Oil & Gas Industry. It features an in-depth coverage of the competitive power of different actor segments. Key players are suppliers, buyers, competitors, new entrants, and substitute product firms. Additionally, it contains an overview of economic data showing the industry market performance over the last 5 years, a statistical forecast for the coming 5 years, key annual financial ratios and key HR data as well as an overview of adopted business strategies of the main companies within the Russian Oil & Gas Industry, including a brief geo-political analysis. The report ends with a general outline of relevant macro-economic indicators and an overview of the main trade associations of the Oil & Gas industry of Russia.

Keywords: Oil, Gas, Russia, competitive intelligence, market intelligence, industry insights, industry profitability, 5 forces analysis, buyer power, supplier power, barriers to entry, competitive rivalry, emerging markets, natural gas, crude oil, energy, exploration & production, distribution & transportation, commodities, electricity, environmental regulation, Covid-19, strategic planning, market volume, market sizing, market assessment, forecasting, foresight, predictive analytics, competitive landscape, competitive environment, threats of substitutes, business strategy, competitive strength, competitive advantage, competitive intensity, threats and opportunities, strengths & weaknesses, SWOT, macroeconomics, political economy, statistics, data analytics, market entry, finance, competition, market opportunities, strategic positioning, developments, performance, business development, strategic alliances, strategic negotiations, bargaining power, sales, research quantitative research, qualitative research, interviewing, surveying, benchmarking, product development, research & development, mergers & acquisitions, pricing, data analytics, data science, segmentation, supply-demand, product development, innovation management, risk

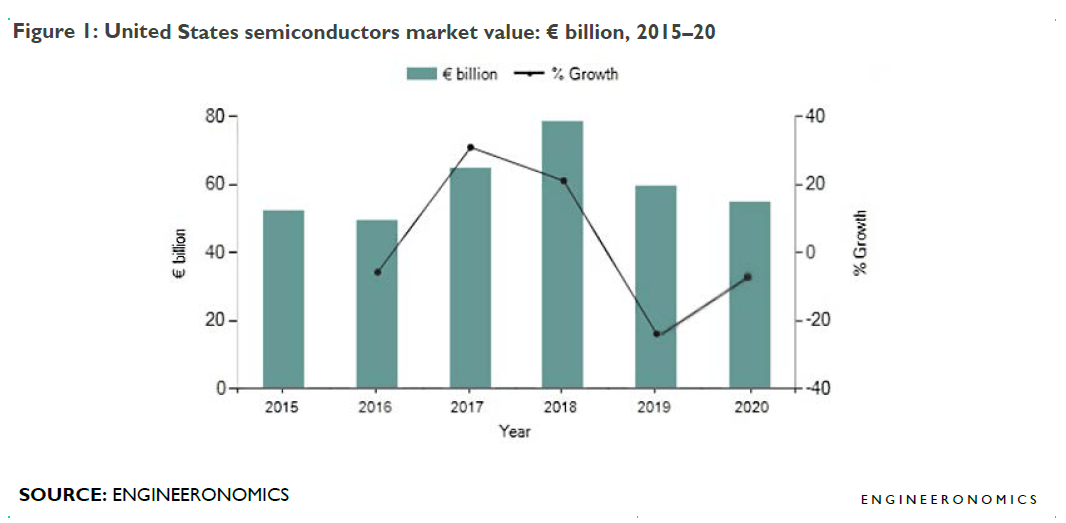

This 49 page market report contains the latest extensive industry assessment of the United States Semiconductor industry. It features an in-depth coverage of the competitive power of key actor segments in the form of the five forces. The five key players are suppliers, buyers, substitute product firms, new entrants, and direct rivals. Additionally, it contains an overview of economic data showing the industry market performance over the last five years, calculated key annual financial ratios of the leading companies, key Human Resources data, as well as an overview of adopted business strategies of the main companies within the US Semiconductor industry. The report ends with a general outline or relevant macro-economic indicators and an overview of the main trade associations of the Semiconductor Industry in the United States.

Keywords: Semiconductor, United States, competitive intelligence, market intelligence, industry insights, industry profitability, 5 forces analysis, buyer power, supplier power, barriers to entry, competitive rivalry, electronics, fabrication, wafer, autonomous driving, Electric Vehicles, Artificial Intelligence, microcontrollers, manufacturing, Virtual Reality, 5G, mobile phones, wireless telecommunication, Covid-19, strategic planning, market volume, market sizing, market assessment, forecasting, foresight, predictive analytics, competitive landscape, competitive environment, threats of substitutes, business strategy, competitive strength, competitive advantage, competitive intensity, profiling, rating, scoring, threats and opportunities, strengths & weaknesses, SWOT, macroeconomics, political economy, statistics, data analytics, market entry, finance, competition, market opportunities, strategic positioning, developments, performance, business development, strategic alliances, strategic negotiations, bargaining power, sales, research quantitative research, qualitative research, interviewing, surveying, benchmarking, product development, research & development, mergers & acquisitions, pricing, data analytics, data science, segmentation, supply-demand, product development, innovation management, risk management, monitoring, equity

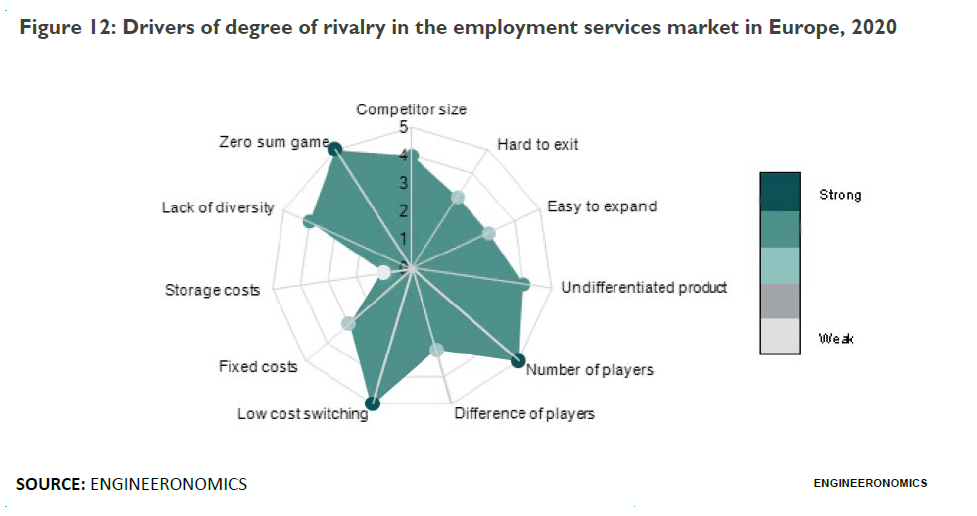

This 57 page industry report contains the latest extensive competitive intelligence analysis of the European Employment Services Industry. It features an in-depth coverage of the competitive power of different actor segments. Key players are suppliers, buyers, competitors, new entrants, and substitute product firms. Additionally, it contains an overview of economic data showing the industry market performance over the last 5 years, a statistical forecast for the coming 5 years, key annual financial ratios and key HR data as well as an overview of adopted business strategies of the main companies within the European Employment Services Industry. The report ends with a general outline of relevant macro-economic indicators and an overview of main trade Associations of the the Employmentservices industry of Europe.

Keywords: Europe, employment services, competitive intelligence, market intelligence, industry insights, industry profitability, 5 forces analysis, buyer power, supplier power, barriers to entry, competitive rivalry, market volume, market sizing, market assessment, forecasting, foresight, predictive analytics, competitive landscape, competitive environment, threats of substitutes, United Kingdom, Germany, France, labor market, recruitment, temporary staffing, search & permanent placement, skills, talent pools, GDPR, online job boards, professional networks, Covid-19, strategic planning, business strategy, competitive strength, competitive advantage, competitive intensity, profiling, scoring, rating, threats and opportunities, strengths & weaknesses, SWOT, macroeconomics, political economy, statistics, data analytics, market entry, finance, competition, market opportunities, strategic positioning, developments, performance, business development, strategic alliances, strategic negotiations, bargaining power, sales, research quantitative research, qualitative research, interviewing, surveying, benchmarking, product development, research & development, mergers & acquisitions, pricing, data analytics, data science, segmentation, supply-demand, product development, innovation management, risk management, monitoring, equity research, investment research, portfolio management, geopolitics

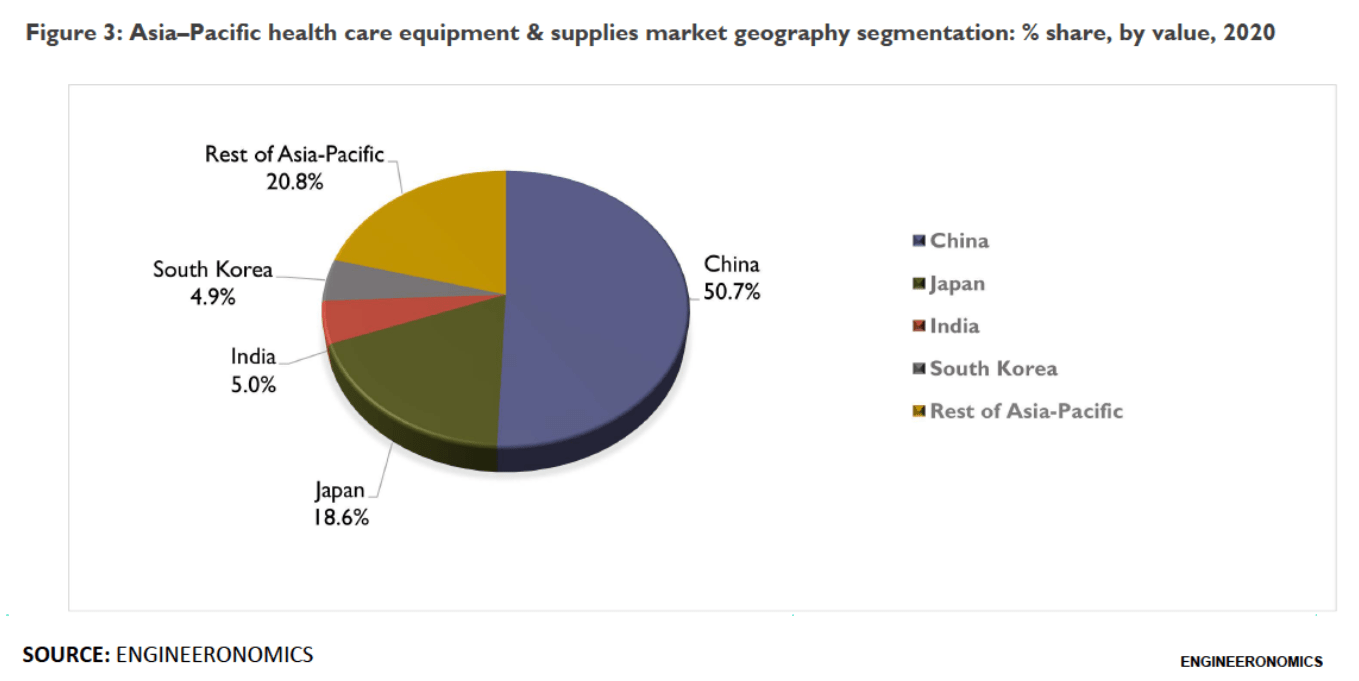

This 34 page industry report contains the latest extensive analysis of the dynamics, trends, threats & opportunities, and a breakdown of product innovations within the Asia Pacific Medical Devices Industry. It features an in-depth coverage of the competitive power of different actor segments. Key players are suppliers, buyers, competitors, new entrants, and substitute product firms. Additionally, it contains an overview of economic data showing the industry market performance over the last 5 years, a statistical forecast for the coming 5 years, as well as an extra separate insight about the Covid-19 impact. The report ends with an overview of adopted business strategies and data belonging to the main companies of the Asia Pacific Medical Technology industry.

Keywords: Asia-Pacific, Medical Technology, competitive intelligence, market intelligence, industry insights, industry profitability, 5 forces analysis, buyer power, supplier power, barriers to entry, competitive rivalry, emerging markets, Asia-Pacific, Japan, China, Singapore, Indonesia, South Korea, Thailand, healthcare, medical, technology, equipment, medical devices, regulation, standards, protocols, disposables, medical imaging, genetic testing, diagnostics, state aid, consumer behavior, smart devices, Covid-19, strategic planning, market volume, market sizing, market assessment, forecasting, foresight, predictive analytics, competitive landscape, competitive environment, threats of substitutes, business strategy, competitive strength, competitive advantage, competitive intensity, profiling, rating, scoring, threats and opportunities, strengths & weaknesses, SWOT, macroeconomics, political economy, statistics, data analytics, market entry, finance, competition, market opportunities, strategic positioning, developments, performance, business development, strategic alliances, strategic negotiations, bargaining power, sales, research quantitative research, qualitative research, interviewing, surveying, benchmarking, product development, research & development, mergers & acquisitions, pricing, data analytics, data science, segmentation, supply-demand, product development, innovation management, risk management, monitoring, equity research, investment research, portfolio management, geopolitics

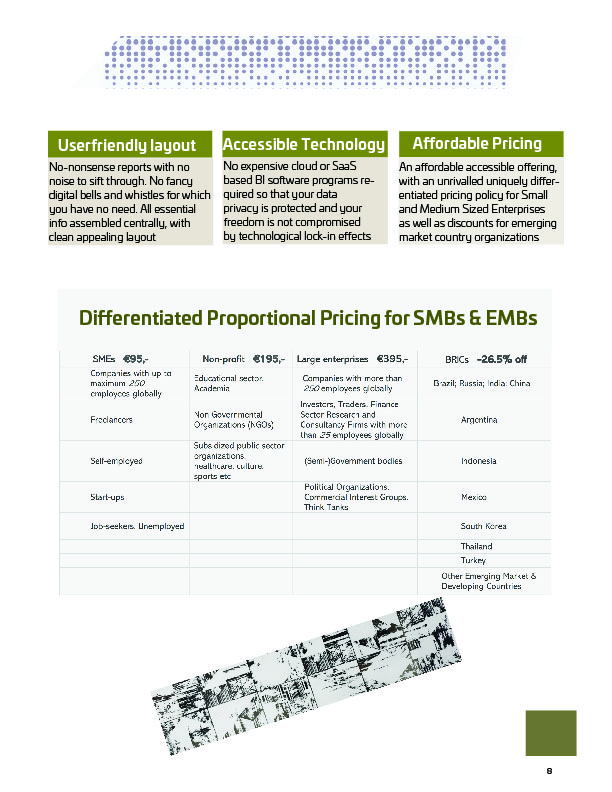

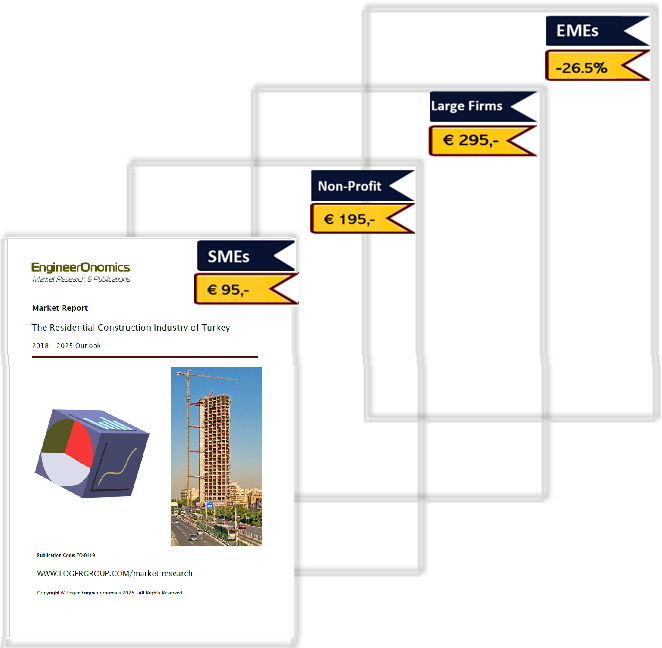

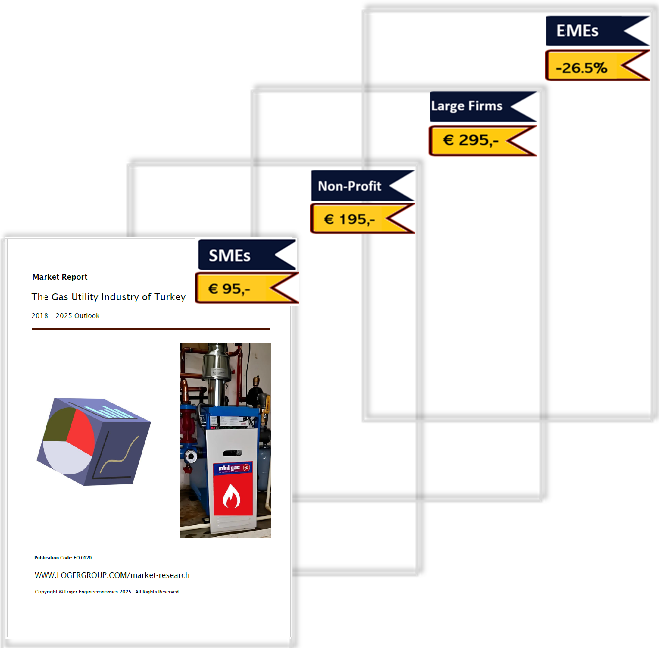

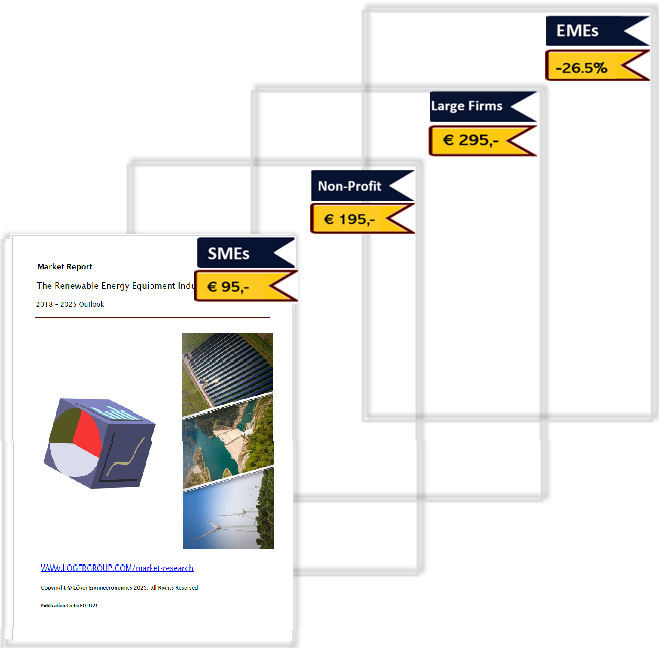

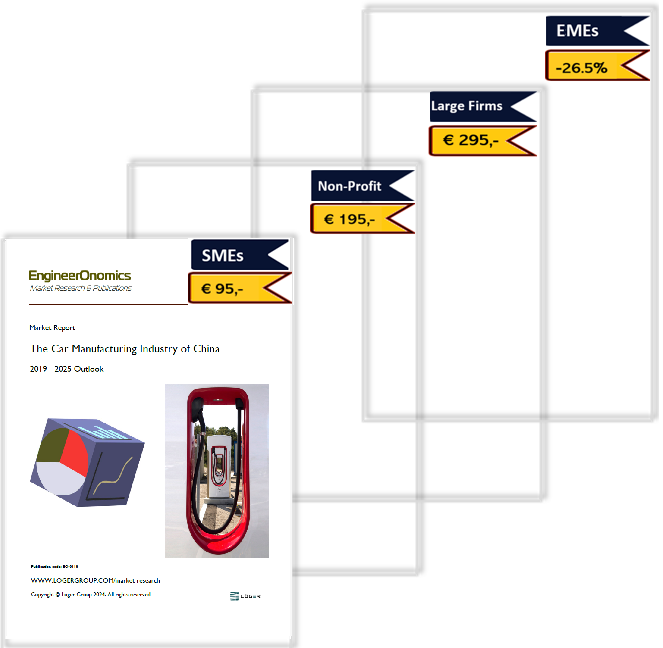

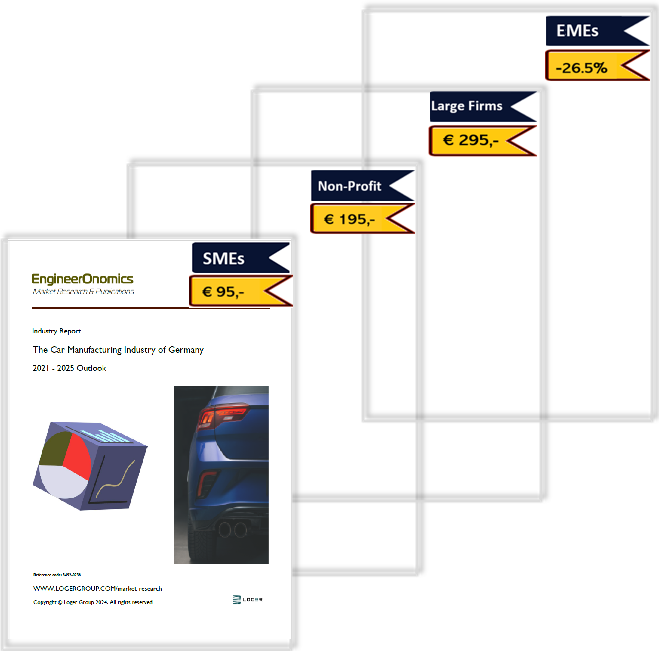

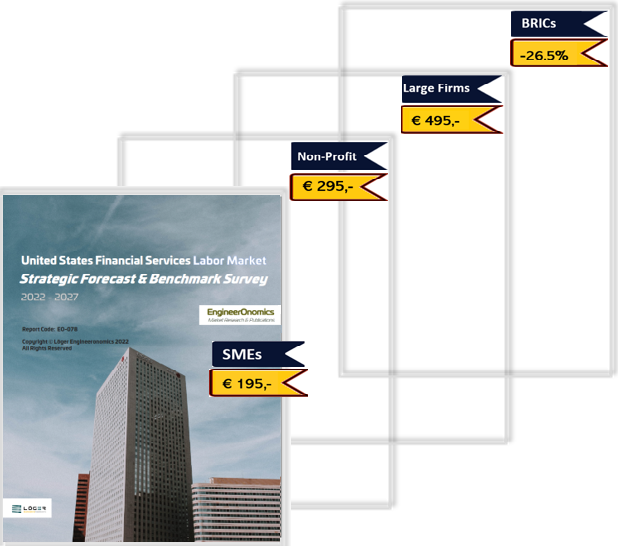

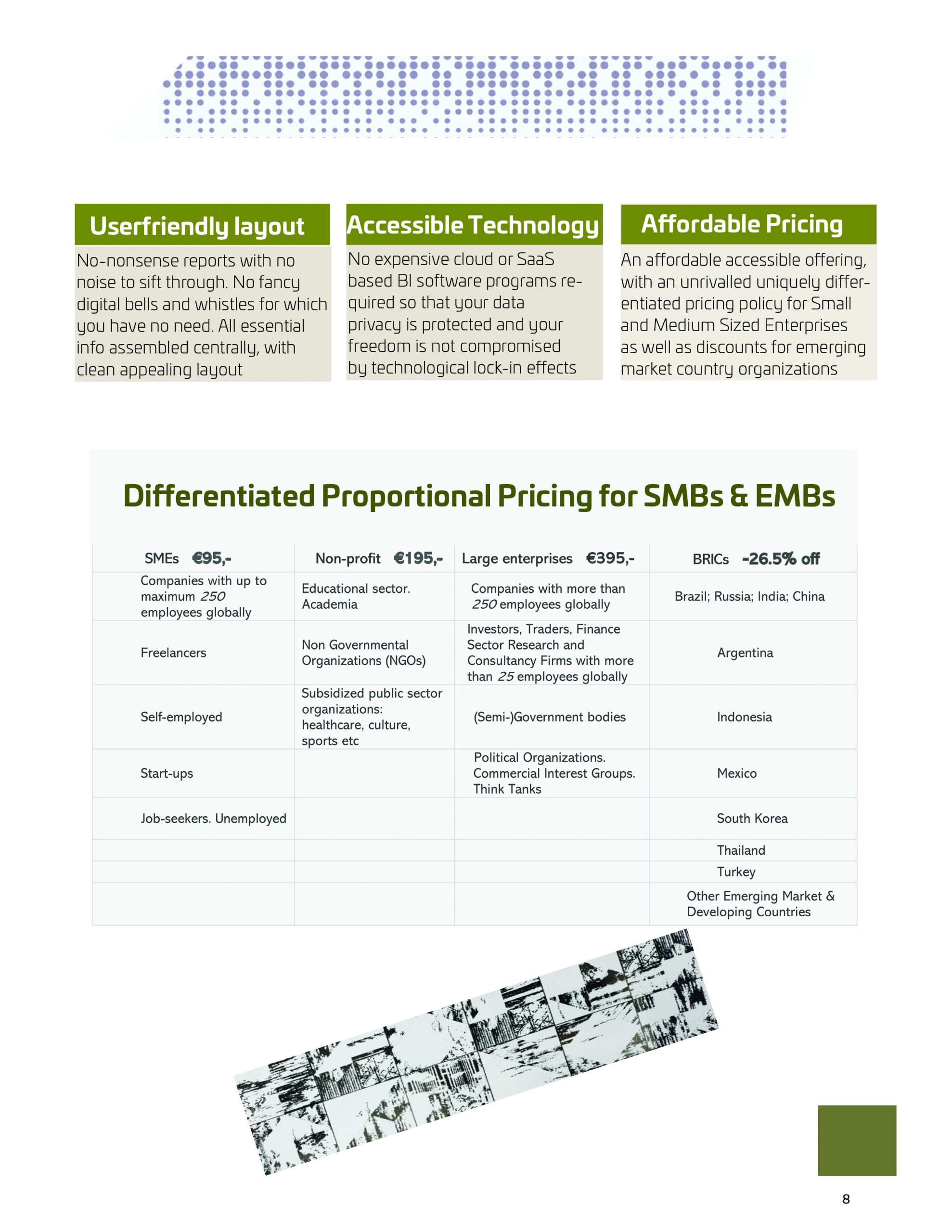

As part of our company philosophy that is based on empowerment and justice, EngineerOnomics Market Research & Publications adopts a differentiated price offering to our different customer segments. Therefore, our reports are sold for €395 to large enterprises, €195 to Non-profit organizations, and €95 to Small and Medium Sized Enterprises (SMEs), excluding TAX/VAT and excluding Paypal transaction fees. There will be an added 26.5% discount for organizations whose headquarters are based in any of the emerging market category countries. Following is an overview of the types of organizations that we consider belonging to each customer category segment.

| SMEs €95 | Non-profit €195 | Large enterprises €395 | BRICs -26.5% off |

|---|---|---|---|

| Companies with up to maximum 250 employees globally | Educational sector. Academia | Companies with more than 250 employees globally | Brazil; Russia; India; China |

| Freelancers | Non-Governmental Organizations (NGOs) | Investors, Traders, Finance Sector Research and Consultancy Firms with more than 25 employees globally | Argentina |

| Self-employed | Subsidized public sector organizations: healthcare, culture, sports etc | (Semi-)Government bodies | Indonesia |

| Start-ups | Political Organizations. Commercial Interest Groups. Think Tanks | Mexico | |

| Job-seekers. Unemployed | South Korea | ||

| Thailand | |||

| Turkey | |||

| Other Emerging Market & Developing Countries |

EngineerOnomics Market Research & Publications© conducts in-house quantitative and qualitative research from which proprietary data are derived and collected. Our primary research methodology consists of interviews and surveys with a variety of market actors including industry professionals, corporate decision makers, SME business owners, academia, and public policy makers.

Interviews are conducted by phone or on-site. We conduct our surveys by utilizing our in-house data collection & assessment portal. Collected data are converted into industry intelligence and publications products. Our data assessment and profiling expertise builds on our candidate assessment and profiling experience that we traditionally use as part of our recruitment assessment activities.

We also use Secondary Research Sources to continuously monitor- and to offer you a more comprehensive view of real time industry developments and trends. The secondary sources that we use are mainly the following:

To process and profile collected data, EngineerOnomics Market Research applies partly an automated process, and largely a manual data assessment method. EngineerOnomics relies on a standardized terminology for the measurements of metrics and the interpretation of data that enables us to create uniform comparisons, calculations, and generalizations across cases, topics, and time. Statistical programs, regression analysis, and institutional economics are some of the tools and frameworks that we employ to build our forecasting models as well as our industry assessments.

Our data modeling, scoring, rating, and financial forecasting tools generate strategic insights, market oversight, and predictive foresights across a variety of key segmentations, levels and units of analysis ranging from macro-economic, industry, subsector, country to region.

EngineerOnomics together with partners are committed to the continuous improvement of data quality and accuracy through a thoroughly validated process of collection, synthesis, and interpretation. Our extensive experience in testing our research techniques and systematic verification, as well as double checking of generated data ensures the reliability of our research results.

EngineerOnomics Market Research & Publications© , part of Löger Group, is specialized in the in-house development and sales of proprietary industry-market reports that deliver competitive intelligence, strategic positioning, and bargaining power to Small- and Medium Sized businesses, Emerging Market Country firms, and beyond. Our reports contain our widely acclaimed Porter's five forces analyses, industry economic forecasts, and key financial ratios about the main players of an industry. Featured economic sectors include engineering intensive and business services oriented industries within a variety of regions.

Our in-house Data Collection portal represents the backbone of our competitive intelligence capabilities, allowing us to conduct market research, assess data, and create data visualizations with scope and scale. The industry-market publications serve as a snapshot scan of your complex competitive landscape, enabling you to anticipate market developments, boost your predictive decision-making and uncover opportunities for strategic alliances. Our affordable external business environment analyses provide you with essential situational awareness to continuously improve your competitive strength and- advantage.

Market research publications help business analysts, researchers, product development professionals, salespeople, and executive level decisionmakers with their strategic planning activities, scenario planning, business development, and investment management. Academia, public officials, NGO's and investors may use our analyses for public policy making purposes, and random professionals can simply use our insights for studying purposes. We sort out key industry measurements for you and package the results in an easy-to-digest standardized visually appealing presentation, accessible from one location. This saves you valuable time, costs, and energy.

It is especially our mission to benefit small- and medium sized enterprises, freelancers, and organizations in emerging countries. Specifically, for smaller entities or entities in emerging market countries we have a differentiated pricing proposition in place that is beneficial from a cost perspective as compared to the prices we charge for larger scale corporate business. Our vision is the objective attainment of truth and the actualization of talent potential and development.

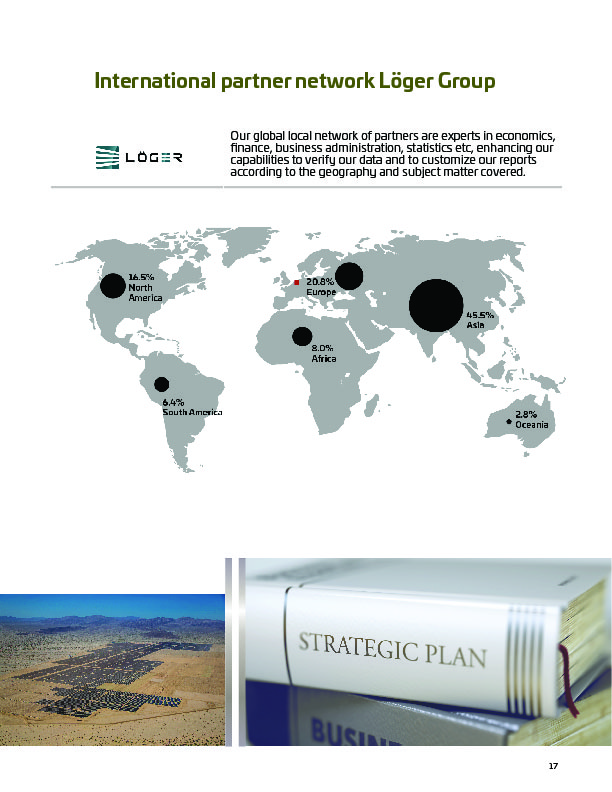

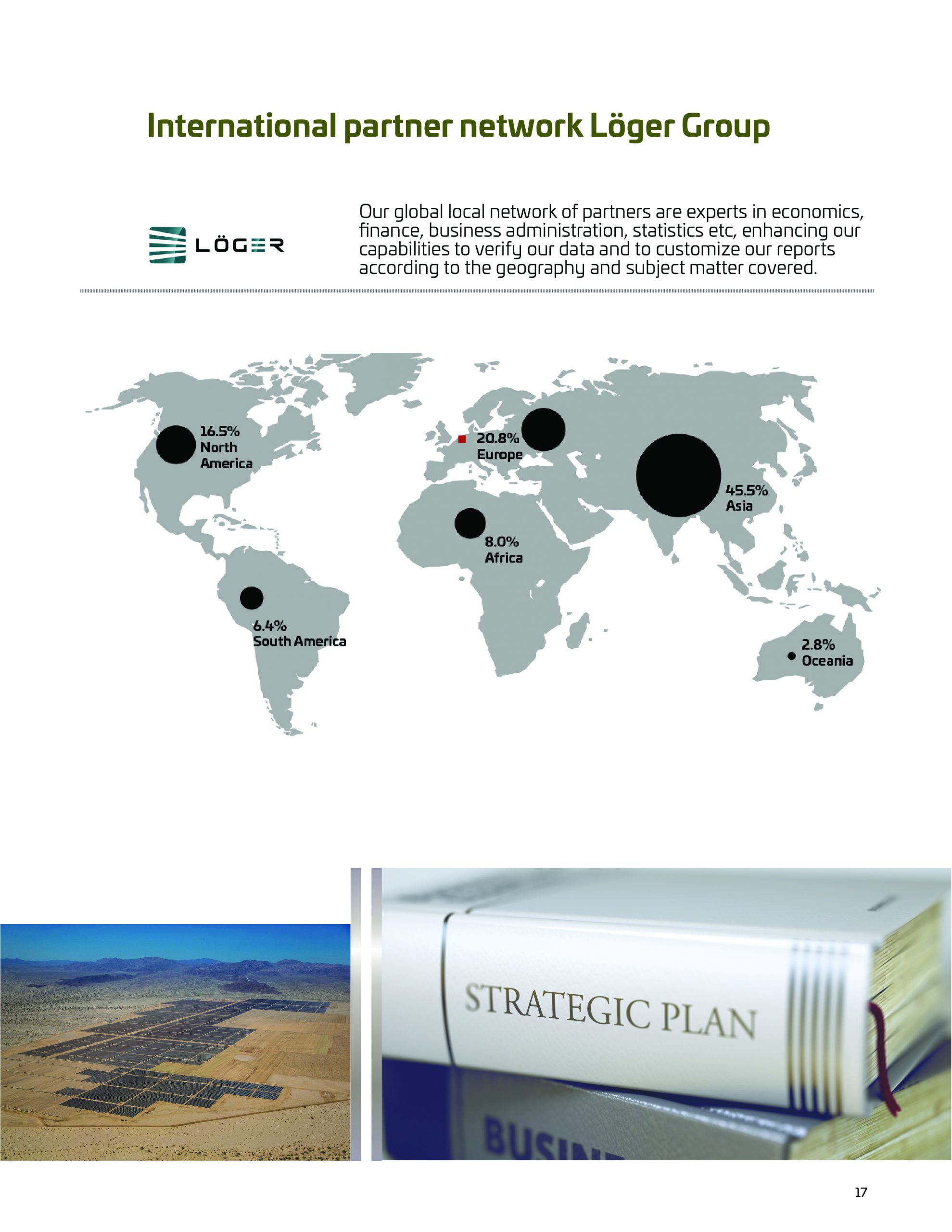

We have over 15 years of industry experience conducting market research, writing and publishing political-economic insights and business development material. Our global local network of partners are experts in economics, finance, business administration and social science, enhancing our capabilities to verify our data and to customize our reports according to the geography and subject matter covered.

Engineeronomics Market Research is part of Löger Group. For further information about our products and services, see more at: https://logergroup.com. For more information about our profile, visit https://logergroup.com/our-profile/. For our EngineerOnomics blog page, see: https://www.logergroup/blog. For contact info visit our contact page at: https://logergroup.com/contact.

All Rights Reserved.

No part of this publication may be reproduced, transmitted, or copied in any way, electronic, mechanical, photocopying, recording or otherwise, without the prior explicit permission of the publisher, EngineerOnomics. The facts of this report are believed to be correct at the time of publication but cannot be guaranteed. Please note that the findings, conclusions, and recommendations that EngineerOnomics delivers will be based on information gathered in good faith from both primary and secondary sources, whose accuracy we are not always able to guarantee. As such EngineerOnomics can accept no liability whatever for actions taken based on any information that may subsequently prove to be incorrect.

Differential proportional pricing policy for SMBs and EMBs

As part of our company philosophy that is based on empowerment and justice, EngineerOnomics Market Research & Publications adopts a differentiated price offering to our different customer segments. Therefore, our reports are sold for €395 to large enterprises, €195 to Non-profit organizations, and €95 to Small and Medium Sized Enterprises (SMEs), excluding TAX/VAT. There will be an added 26.5% discount for organizations whose headquarters are based in any of the Emerging Market Enterprises (EMEs). Following is an overview of the types of organizations that we consider belonging to each customer category segment.

| SMEs €95 | Non-profit €195 | Large enterprises €395 | EMEs -26.5% off |

|---|---|---|---|

| Companies with up to maximum 250 employees globally | Educational sector. Academia | Companies with more than 250 employees globally | Brazil; Russia; India; China |

| Freelancers | Non-Governmental Organizations (NGOs) | Investors, Traders, Finance Sector Research and Consultancy Firms with more than 25 employees globally | Argentina |

| Self-employed | Subsidized public sector organizations: healthcare, culture, sports etc | (Semi-)Government bodies | Indonesia |

| Start-ups | Political Organizations. Commercial Interest Groups. Think Tanks | Mexico | |

| Job-seekers. Unemployed | South Korea | ||

| Thailand | |||

| Turkey | |||

| Other Emerging Market & Developing Countries |

EngineerOnomics Market Research & Publications© conducts in-house quantitative and qualitative research from which proprietary data are continuously derived and collected. Our primary research methodology consists of interviews and surveys with a variety of market actors including industry professionals, corporate decision makers, SME business owners, academia, and public policy makers.

Interviews are conducted by phone or on-site. We conduct our surveys by utilizing our in-house data collection & assessment portal. Collected data are converted into industry intelligence and publications products. Our data assessment and profiling expertise builds on our candidate assessment and profiling experience that we traditionally use as part of our recruitment assessment activities.

We also use Secondary Research Sources to continuously monitor- and to offer you a more comprehensive view of real time industry developments and trends. The secondary sources that we use are mainly the following:

To process and profile collected data, EngineerOnomics Market Research applies partly an automated process, and largely a manual data assessment method. EngineerOnomics relies on a standardized terminology for the measurements of metrics and the interpretation of data that enables us to create uniform comparisons, calculations, and generalizations across cases, topics, and time. Statistical programs, regression analysis, and institutional economics are some of the tools and frameworks that we employ to build our forecasting models as well as our industry assessments.

Our data modeling, scoring, rating, and financial forecasting tools generate strategic insights, market oversight, and predictive foresights across a variety of key segmentations, levels and units of analysis ranging from macro-economic, industry, subsector, country to region.

EngineerOnomics together with partners are committed to the continuous improvement of data quality and accuracy through a thoroughly validated process of collection, synthesis, and interpretation. Our extensive experience in testing our research techniques and systematic verification, as well as double checking of generated data ensures the reliability of our research results.

EngineerOnomics Market Research & Publications© , part of Löger Group, is specialized in the continious proprietary development and sales of proprietary industry-market reports that deliver competitive intelligence, strategic positioning, and bargaining power to Small- and Medium Sized businesses, Emerging Market Country firms, and beyond. Our reports contain our widely acclaimed Porter's five forces analyses, industry economic forecasts, and key financial ratios about the main players of an industry. Featured economic sectors include engineering intensive and business services oriented industries within a variety of regional markets. Additionally , we publish strategic labor market- as well as career management studies that contain avanced - commercial data driven - strategic mapping, forecasting, scenario assessment, Strategic Human Resource Management (SHRM) and Innovation Manageement (IM), profiling analyses etc.

Our in-house Data Collection portal represents the backbone of our competitive intelligence capabilities, allowing us to conduct market research, assess data, and create data visualizations with scope and scale. The industry-market publications serve as a snapshot scan of your complex competitive landscape, enabling you to anticipate market developments, boost your predictive decision-making and uncover opportunities for strategic alliances. Our affordable external business environment analyses provide you with essential situational awareness to continuously improve your competitive strength and- advantage.

Market research publicationshelp business analysts, researchers, product development professionals, salespeople, and executive level decisionmakers with their strategic planning activities, scenario planning, business development, and investment management. Academia, public officials, NGO's and investors may use our analyses for public policy making purposes, and random professionals can simply use our insights for studying purposes. We sort out key industry measurements for you and package the results in an easy-to-digest standardized visually appealing presentation, accessible from one location. This saves you valuable time, costs, and energy.

It is especially our mission to benefit small- and medium sized enterprises (SMEs), freelancers, and organizations in emerging countries. Specifically, for smaller business entities or entities in emerging market countries we have a differentiated pricing proposition in place that is beneficial from a cost perspective as compared to the prices we charge for larger scale corporate business. Our vision is the objective attainment of truth and the actualization of talent potential and development.

Our background consists of over 15 years of industry experience conducting market research, writing and publishing political-economic insights and business development material. Our global local network of partners are experts in economics, finance, business administration and social science, enhancing our capabilities to verify our data and to customize our reports according to the geography and subject matter covered.

Engineeronomics Market Research is part of Löger Group. For further information about our products and services, see more at: https://logergroup.com. For more information about our profile, visit https://logergroup.com/our-profile/. For our EngineerOnomics blog page, see: https://logergroup.com/blog. For contact info visit our contact page at: https://logergroup.com/contact.

All Rights Reserved.

No part of this publication may be reproduced, transmitted, or copied in any way, electronic, mechanical, photocopying, recording or otherwise, without the prior explicit permission of the publisher, EngineerOnomics. The facts of this report are believed to be correct at the time of publication but cannot be guaranteed. Please note that the findings, conclusions, and recommendations that EngineerOnomics delivers will be based on information gathered in good faith from both primary and secondary sources, whose accuracy we are not always able to guarantee. As such EngineerOnomics can accept no liability whatever for actions taken based on any information that may subsequently prove to be incorrect.